Xuguang Simon Sheng is a Professor of Economics at American University. He currently serves as the chair of the Department of Economics and the editor of International Review of Economics & Finance. His research interests include time series econometrics, machine learning, monetary policy, fiscal policy, energy policy, forecasting, measuring uncertainty and survey expectations.

He has published in Journal of Econometrics, Journal of Applied Econometrics, Review of Economics and Statistics, European Economic Review, Journal of Money, Credit and Banking, Journal of International Monetary and Finance, Journal of Accounting and Economics, Energy Economics and the Oxford Handbook on Economic Forecasting.

He has received the IIF-SAS Award from International Institute of Forecasters and SAS® in 2023, Isaac Kerstenetzky Award from Fundação Getulio Vargas (FGV) of Brazil in 2021 and Heinz König Young Scholar Award from Centre for European Economic Research (ZEW) of Germany in 2010. He has served as an associate editor for International Journal of Forecasting and Oxford Open Economics, a guest editor for Energy Economics (2023, titled "Inflation Dynamics in a New Era of Energy Price Shocks"), International Journal of Forecasting (2022, titled "Economic Forecasting in Times of Covid-19," and 2019, titled "Forecasting Issues in Developing Economies"), and Journal of International Money and Finance (2025, titled "Uncertainty and Economic Activity"), and a co-organizer of ten international conferences.

What's New

Working Papers

• Economic Policy Uncertainty in China Since 1949: The View from Mainland Newspapers, with Steve Davis and Dingqian Liu. Data on China EPUPresented at: IMF, SEA, 2nd Applied Macroeconomics Forum

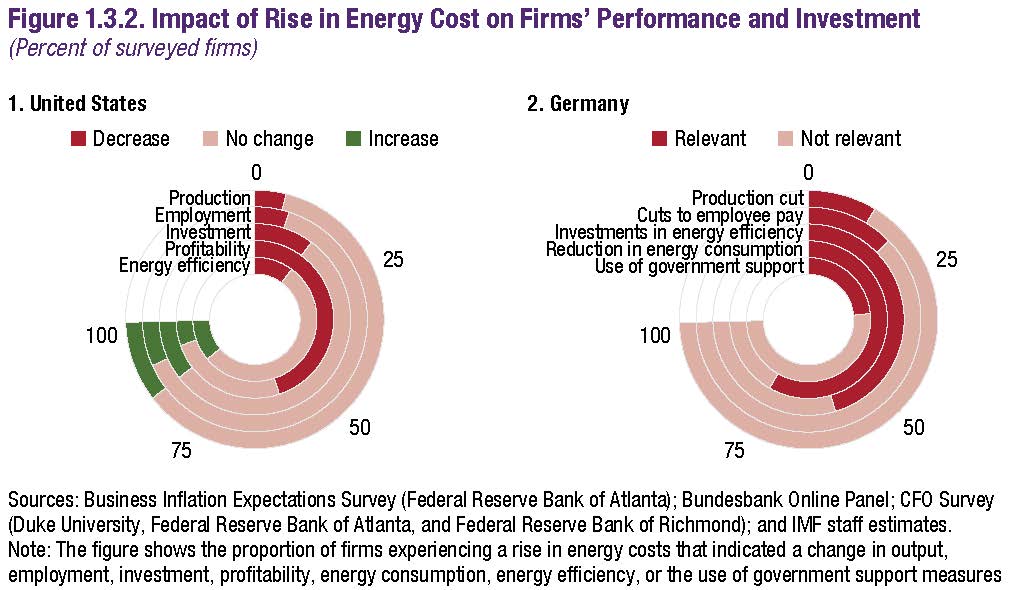

• Firms' Resilience to Energy Shocks and Response to Fiscal Incentives: Assessing the Impact of 2022 Energy Crisis, with David Amaglobeli, Joaquim Guilhoto, Samir Jahan, Salma Khalid, Waikei Lam, Gregory Legoff, Brent Meyer, Pawel Smietanka, Sonya Waddell, and Daniel Weitz. IMF Working Paper No. 2024/27

Presented at: IMF

Publications

Presented at: Joint Statistical Meetings, 25th Federal Forecasters Conference, 29th International Panel Data Conference, 45th International Symposium on Forecasting, and 5th Annual DC-MD-VA Econometrics Workshop

Presented at: Cleveland Fed, Philadelphia Fed, Federal Reserve Board, IWH-CIREQ-GW, FFC, ESCoE, IMF, ISF, IAAE, CEBRA, CIRET, ICEA, OeNB Conference, Video (starting at 52:00), George Washington University, Renmin University of China, University College Dublin, Pennsylvania State University and Stanford University

Supported by the IIF-SAS Award

Presented at: 43rd International Symposium on Forecasting, 5th Behavioral Macroeconomics Workshop, Central Bank Research Association 2023 Annual Meeting, Conference on “Inflation Dynamics in a New Era of Energy Price Shocks”, and George Washington University

Presented at: 43rd International Symposium on Forecasting, George Washington University

• Inattention and the Impact of Monetary Policy, with Zidong An and Salem Abo-Zaid (2023), Journal of Applied Econometrics, vol. 38, pp. 623-643.

Presented at: AEA, IAAE, FFC, ISF, National Bank of Poland, George Washington University and American University

• Disagreement in Consumer Inflation Expectations, with Tomasz Lyziak (2023), Journal of Money, Credit and Banking, vol. 55, pp. 2215-2241.

Presented at: CFE, GCER

• Stock Prices and Economic Activity in the Time of Coronavirus, with Steve Davis and Dingqian Liu (2022), IMF Economic Review, vol. 70, pp. 32-67.

• Term Structure of Uncertainty: New Evidence from Survey Expectations, with Carola Binder and Tucker McElroy (2022), Journal of Money, Credit and Banking, vol. 54, pp. 39-71.

• Measuring Uncertainty of a Combined Forecast and Some Tests for Forecaster Heterogeneity, with Kajal Lahiri and Huaming Peng (2022), In A. Chudik, C. Hsiao and A. Timmermann (eds.), Advances in Econometrics, Essays in Honor of Hashem Pesaran: Prediction and Macro Modeling, vol. 43A, pp. 29-50.

• The Impact of the COVID-19 Pandemic on Business Expectations, with Brent Meyer and Brian Prescott (2022), International Journal of Forecasting, vol. 38, pp. 529-544.

• Identifying External Debt Shocks in Low- and Middle-Income Countries, with Rubena Sukaj (2021), Journal of International Money and Finance, vol. 110, pp. 1-17.

• Dating COVID-Induced Recession in the U.S., with Haixi Li (2021), Applied Economics Letters, vol. 28, pp. 1723-1727.

• Monitoring Recessions: A Bayesian Sequential Quickest Detection Method, with Haixi Li and Jingyun Yang (2021), International Journal of Forecasting, vol. 37, pp. 500-510.

• Expectation Formation Following Large Unexpected Shocks, with Scott Baker and Tucker McElroy (2020), Review of Economics and Statistics, vol. 102, pp. 287-303.

• Do Managers Use Earnings Forecasts to Fill a Demand They Perceive from Analysts?, with Orie Barron, Jian Cao, Maya Thevenot and Baohua Xin (2020), In C.F. Lee and J.C. Lee (eds.), Handbook of Financial Econometrics, Mathematics, Statistics, and Machine Learning, pp. 101-149, World Scientific.

• The Measurement and Transmission of Macroeconomic Uncertainty: Evidence from the U.S. and BRIC Countries, with Yang Liu (2019), International Journal of Forecasting, vol. 35, pp. 967-979.

• Measuring Global and Country-specific Uncertainty, with Ezgi Ozturk (2018), Journal of International Money and Finance, vol. 88: 276-295. Data on global uncertainty

• Combinations of “Combinations of P-values”, with Lan Cheng (2017), Empirical Economics, vol. 53, pp. 329-350.

• Measuring Disagreement in Qualitative Expectations, with Frieder Mokinski and Jingyun Yang (2015), Journal of Forecasting, vol. 34, pp. 405-426.

• Quantifying Differential Interpretation of Public Information Using Financial Analysts’ Earnings Forecasts, with Maya Thevenot (2015), International Journal of Forecasting, vol. 31, pp. 515-530.

• Evaluating the Economic Forecasts of FOMC Members, (2015), International Journal of Forecasting, vol. 31, pp. 165-175.

• Truncated Product Methods for Panel Unit Root Tests, with Jingyun Yang (2013), Oxford Bulletin of Economics and Statistics, vol. 75, pp. 624-636.

• An Adaptive Truncated Product Method for Combining Dependent P-values, with Jingyun Yang (2013), Economics Letters, vol. 119, pp. 180-182.

• A New Measure of Earnings Forecast Uncertainty, with Maya Thevenot (2012), Journal of Accounting and Economics, vol. 53, pp. 21-33.

• Analyzing Three-dimensional Panel Data of Forecasts, with Antony Davies and Kajal Lahiri (2011), in M.P. Clements and D.F. Hendry (eds.), Oxford Handbook on Economic Forecasting, pp. 473-495, Oxford University Press.

• Panel Unit Root Tests by Combining Dependent P-values: A Comparative Study, with Jingyun Yang (2011), Journal of Probability and Statistics, vol. 2011, Article ID 617652, 17 pages.

• Measuring Forecast Uncertainty by Disagreement: The Missing Link, with Kajal Lahiri (2010), Journal of Applied Econometrics, vol. 25, pp. 514-538.

• Learning and Heterogeneity in GDP and Inflation Forecasts, with Kajal Lahiri (2010), International Journal of Forecasting, vol. 26, pp. 265-292.

• Evolution of Forecast Disagreement in a Bayesian Learning Model, with Kajal Lahiri (2008), Journal of Econometrics, vol. 144, pp. 325-340.

Organized Conferences

• Workshop on Uncertainty, Economic Activity, and Policy, Warsaw, Poland, June 19–20, 2026• 6th Annual DC-MD-VA Econometrics Workshop in Washington, DC, September 20, 2025

• 4th Applied Macroeconomics Forum on "Climate Policy, Commodity Markets, and Economic Adaptations", Shenzhen, China, June 25-26, 2025

• Sixth Biennial Conference on Uncertainty and Risk in Macroeconomics: Decision Making and Policy Challenges, Marseille, France, June 12-13, 2025

• Fifth Biennial Conference on Uncertainty, Economic Activity, and Forecasting in a Changing Environment, Padua, Italy, September 21-22, 2023

• Conference on Inflation Dynamics in a New Era of Energy Price Shocks, Online, November 11-12, 2022

• Fourth Biennial Conference on Uncertainty and Economic Activity: Global Perspectives, Online, May 13-14, 2021

• Third Biennial Conference on Uncertainty and Economic Activity: Measurement, Facts and Fiction, Beijing, China, May 10-11, 2018

• Second Biennial Conference on Impact of Uncertainty Shocks on the Global Economy, London, UK, May 12-13, 2016

• First Biennial Conference on Uncertainty and Economic Forecasting, London, UK, May 8-9, 2014

• 26th International Institute of Forecasters Workshop on Economic Forecasting in Times of Covid-19, Online, July 6-7, 2020

• 21st International Institute of Forecasters Workshop on Forecasting Issues in Developing Economies, Washington, DC, US, April 26-27, 2017